Abstract

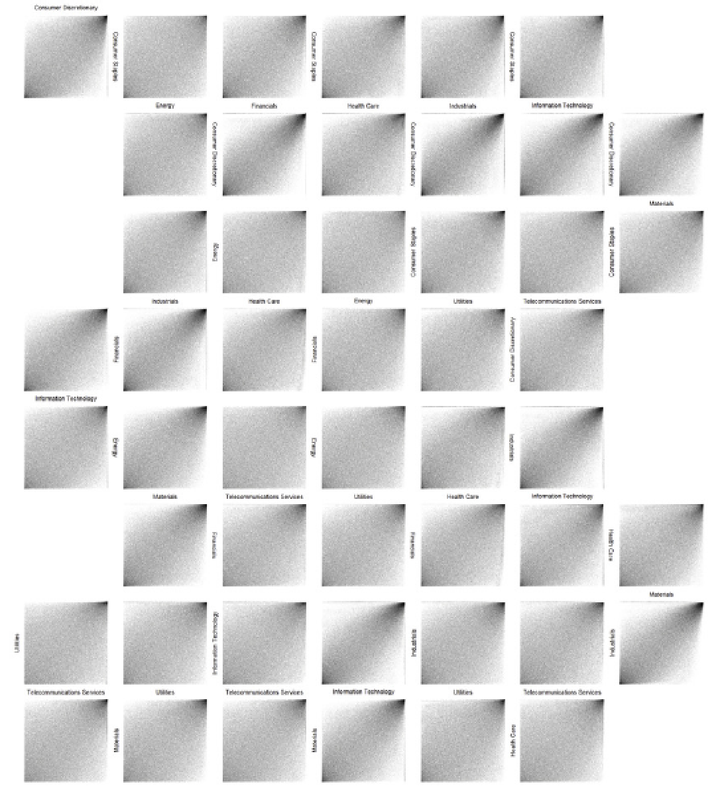

A framework for quantifying dependence between random vectors is introduced. Using the notion of a collapsing function, random vectors are summarized by single random variables, referred to as collapsed random variables. Measures of association computed from the collapsed random variables are then used to measure the dependence between random vectors. To this end, suitable collapsing functions are presented. Furthermore, the notion of a collapsed distribution function and collapsed copula are introduced and investigated for certain collapsing functions. This investigation yields a multivariate extension of the Kendall distribution and its corresponding Kendall copula for which some properties and examples are provided. In addition, non-parametric estimators for the collapsed measures of association are provided along with their corresponding asymptotic properties. Finally, data applications to bioinformatics and finance are presented along with a general graphical assessment of independence between groups of random variables.